For improved accountability, the Code of Governance for Charities and Institutions of a Public Character (IPC) aims to set out principles and best practices in governance and transparency of charities in Singapore. Charities and IPCs should apply the refined Code for financial year commencing from 1 January 2018.

Five key refinements in the Code 2017 include the principle of comply or explain, definition of charity size, changes in tiered guideline, the introduction of an intermediate tier, and greater disclosure for board members.

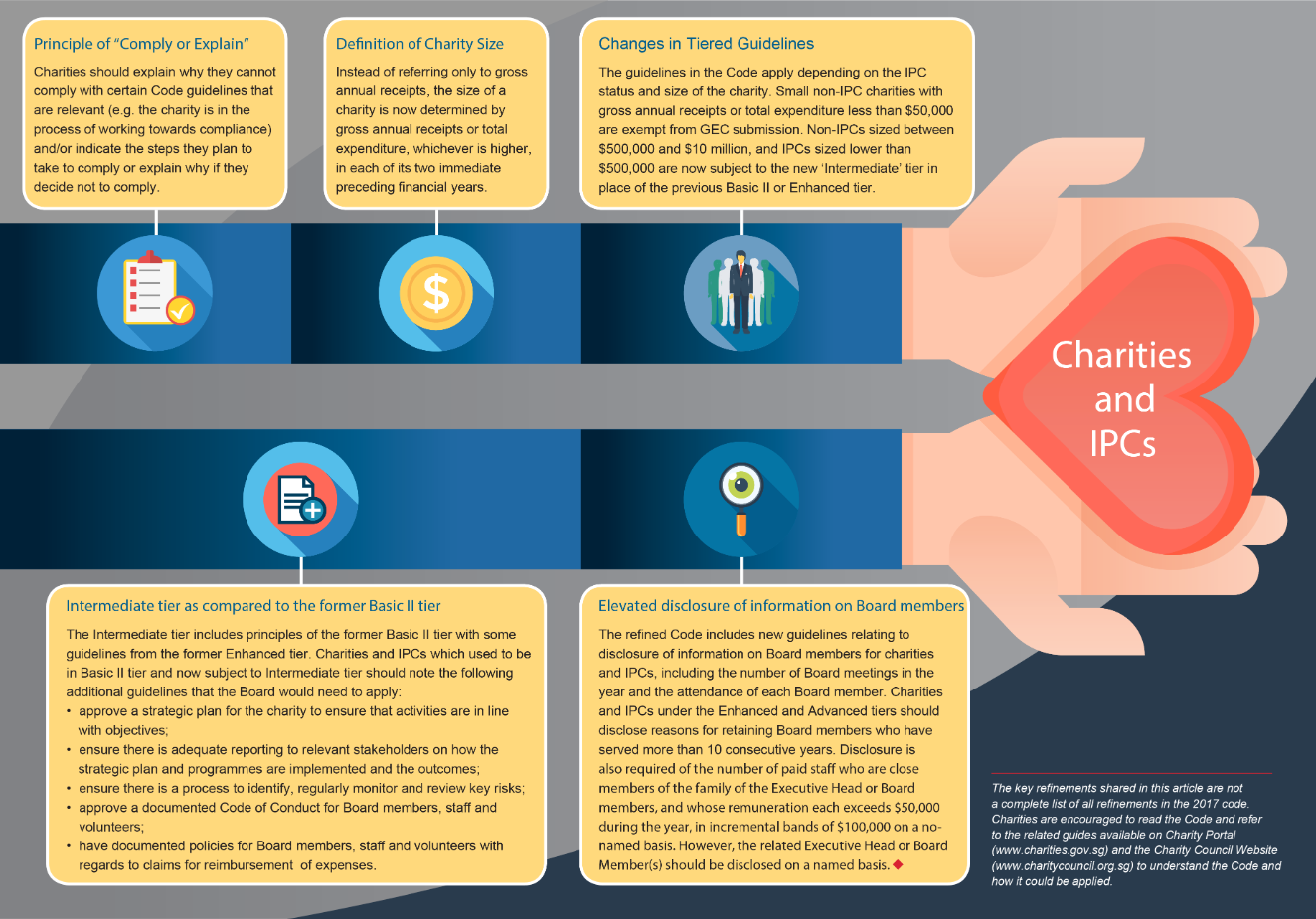

Principle of “Comply or Explain”

Charities should explain why they cannot comply with certain Code guidelines that are relevant (e.g. the charity is in the process of working towards compliance) and/or indicate the steps they plan to take to comply or explain why if they decide not to comply.

Definition of Charity Size

Instead of referring only to gross annual receipts, the size of a charity is now determined by gross annual receipts or total expenditure, whichever is higher, in each of its two immediate preceding financial years.

Changes in Tiered Guidelines

The guidelines in the Code apply depending on the IPC status and size of the charity. Small non-IPC charities with gross annual receipts or total expenditure less than $50,000 are exempt from GEC submission. Non-IPCs sized between $500,000 and $10 million, and IPCs sized lower than $500,000 are now subject to the new ‘Intermediate’ tier in place of the previous Basic II or Enhanced tier.

Intermediate tier as compared to the former Basic II tier

The Intermediate tier includes principles of the former Basic II tier with some guidelines from the former Enhanced tier. Charities and IPCs which used to be in Basic II tier and now subject to Intermediate tier should note the following additional guidelines that the Board would need to apply:

- approve a strategic plan for the charity to ensure that activities are in line with objectives;

- ensure there is adequate reporting to relevant stakeholders on how the strategic plan and programmes are implemented and the outcomes;

- ensure there is a process to identify, regularly monitor and review key risks;

- approve a documented Code of Conduct for Board members, staff and volunteers;

- have documented policies for Board members, staff and volunteers with regards to claims for reimbursement of expenses.

Elevated disclosure of information on Board members

The refined Code includes new guidelines relating to disclosure of information on Board members for charities and IPCs, including the number of Board meetings in the year and the attendance of each Board member. Charities and IPCs under the Enhanced and Advanced tiers should disclose reasons for retaining Board members who have served for more than 10 consecutive years. Disclosure is also required of the number of paid staff who are close members of the family of the Executive Head or Board members, and whose remuneration each exceeds $50,000 during the year, in incremental bands of $100,000 on a no-named basis. However, the related Executive Head or Board Member(s) should be disclosed on a named basis.

The key refinements shared in this article are not a complete list of all refinements in the 2017 Code. Charities are encouraged to read the Code and refer to the related guides available on Charity Portal (www.charities.gov.sg) and the Charity Council Website (www.charitycouncil.org.sg) to understand the Code and how it could be applied.

DISCLAIMER: All opinions, conclusions, or recommendations in this article are reasonably held by Baker Tilly at the time of compilation but are subject to change without notice to you. Whilst every effort has been made to ensure the accuracy of the contents in this article, the information in this article is not designed to address any particular circumstance, individual or entity. Users should not act upon it without seeking professional advice relevant to the particular situation. We will not accept liability for any loss or damage suffered by any person directly or indirectly through reliance upon the information contained in this article.

Related content